Financial services IT compliance: a 2026 guide for professionals

TL;DR:

- Financial services IT compliance involves managing controls to meet regulatory standards like SOX and NIST. Automated RegTech solutions enable continuous monitoring, reduce audit workload, and improve control effectiveness. Maintaining up-to-date asset and access data is essential for compliance and audit readiness.

Financial services IT compliance is defined as the ongoing practice of implementing, managing, and evidencing IT general controls (ITGCs) to satisfy the regulatory obligations that govern how financial institutions process, store, and report data. The discipline sits at the intersection of technology governance and regulatory adherence, covering frameworks such as the Sarbanes-Oxley Act (SOX), NIST SP 800-53 Rev 5, and FCA rules. For IT compliance professionals in financial services, the stakes are concrete: a single control deficiency in access management or log retention can trigger an audit finding, a regulatory sanction, or a material weakness disclosure. The function has moved well beyond annual checkbox reviews. Continuous monitoring, automated evidence collection, and risk-based control mapping now define what good looks like in 2026.

What are the key regulatory requirements for financial services IT compliance?

SOX Section 404 is the most operationally demanding requirement for IT teams in listed financial institutions. It mandates documentation, testing, and ongoing validation of Internal Controls over Financial Reporting (ICFR), covering every IT system that touches financial data, including ERP platforms, billing systems, and revenue recognition tools. The implication is direct: if a system produces a number that appears in a financial statement, it falls within SOX scope.

NIST SP 800-53 Rev 5 provides the most comprehensive control catalogue available to financial institutions. The framework covers 192 security controls across 22 domains and maps directly to regulators including the SEC, FCA, and MAS. That cross-mapping capability is its primary value. Financial institutions operating across multiple jurisdictions use it to reduce duplicated control work and close regulatory gaps in a single pass.

Beyond SOX and NIST, the regulatory perimeter for IT compliance in finance is wide. Key frameworks include:

- FCA rules governing operational resilience and systems integrity for UK-regulated firms

- GLBA (Gramm-Leach-Bliley Act) requiring safeguards for customer financial data in the US

- PCI DSS applying to any system that processes payment card data

- GDPR imposing data protection controls on any system holding EU personal data

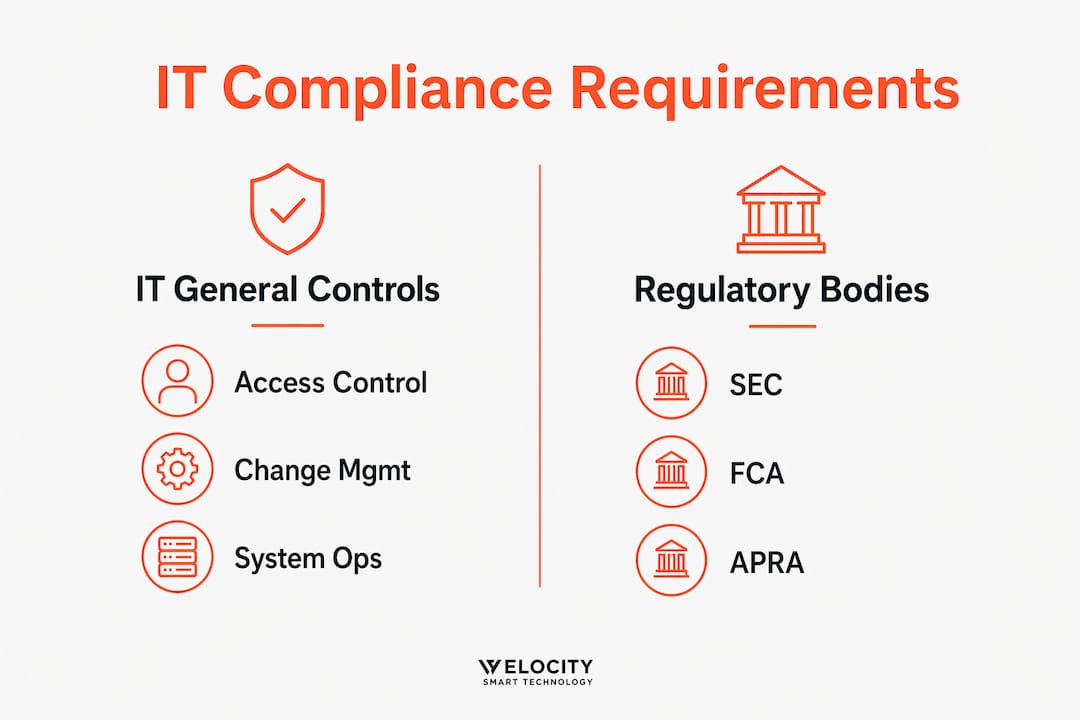

Each regulation targets a different layer of the IT estate, but they share a common dependency on four ITGC domains:

| ITGC domain | Core compliance requirement |

|---|---|

| Logical access controls | Role-based access, least privilege, quarterly reviews |

| Change management | Documented authorisation, testing, and dev/prod separation |

| System operations | Monitoring, incident response, and availability controls |

| Data centre security | Physical and environmental controls for financial systems |

Financial institutions face overlapping regulator requirements across SEC, FCA, APRA, and MAS simultaneously. A unified control framework reduces the compliance burden and the risk of gaps between jurisdictions.

How do RegTech and automation transform IT compliance in finance?

Financial services regulatory technology (RegTech) has shifted from a niche category to a core compliance infrastructure component. Advanced RegTech platforms monitor over 3 million regulatory data points from more than 2,000 sources across 160+ jurisdictions in real time. That scale of surveillance is not achievable through manual processes. The practical output is automated obligation-to-control mapping: when a regulation changes, the platform flags the affected controls immediately rather than waiting for the next audit cycle.

The operational benefits of mature RegTech adoption are measurable across three dimensions:

- Reduced audit fatigue: automated evidence collection replaces manual document assembly, cutting audit cycle times and reducing the volume of auditor requests

- Proactive risk management: continuous monitoring surfaces control failures before they become audit findings

- Regulatory agility: horizon scanning tools alert compliance teams to incoming rule changes, giving IT teams lead time to adjust controls

The challenge is integration. Most financial institutions run legacy core banking systems that were not designed for API-driven compliance tooling. Connecting a modern RegTech platform to a 15-year-old payment processing system requires careful data mapping and often a middleware layer. Teams that underestimate this integration effort typically see delayed deployments and incomplete data feeds, which undermine the continuous monitoring value proposition.

Pro Tip: Before selecting a RegTech tool, map every financial system in scope against its data output format. Platforms that cannot ingest your existing log and event data natively will require custom connectors that add cost and maintenance overhead.

What are the common pitfalls in maintaining financial IT compliance?

The most frequently cited control deficiency in SOX audits is insufficient access review frequency. Auditors expect quarterly access reviews to verify adherence to the principle of least privilege. Many organisations conduct these reviews annually, which leaves months of undetected privilege creep between assessments. That gap is where audit findings originate.

Log retention is the second most common failure point. System logs must be retained securely for up to seven years to meet SOX audit evidence requirements. Many organisations retain logs for only 90 days, often because default cloud storage configurations are not adjusted at deployment. The result is an audit request for evidence that no longer exists.

The following pitfalls account for the majority of material control weaknesses in financial services IT environments:

- Infrequent access reviews: Annual reviews fail to detect privilege creep between cycles. Quarterly reviews are the auditor-expected standard.

- Weak change management controls: Documented authorisation and dev/prod separation are required for every code change touching financial systems. CI/CD pipelines that bypass these gates create direct audit exposure.

- SaaS sprawl: Each new SaaS application added to the financial IT estate extends the ITGC perimeter. Compliance teams that do not track SaaS adoption in real time accumulate unreviewed systems.

- Segregation of duties conflicts: Developers who also hold production access can push unauthorised code to financial reporting systems. This is a significant DevOps compliance risk that many fast-moving engineering teams do not address until an auditor raises it.

- Incomplete evidence packages: Point-in-time assessments do not satisfy modern audit standards. Continuous monitoring and evidence collection throughout the financial year are required.

Pro Tip: Run a quarterly “shadow audit” using your own control testing procedures before the external auditor arrives. Teams that do this consistently reduce the volume of auditor requests by a material margin and avoid the scramble for evidence at year-end.

Dynamic IT environments compound every one of these risks. Cloud-native deployments, containerised workloads, and CI/CD pipelines change the IT estate faster than annual control assessments can track. The compliance programme must match the pace of the technology environment, not the pace of the audit calendar.

What best practices ensure ongoing regulatory adherence in financial IT?

Embedding ITGCs early in the development lifecycle is the single most effective way to reduce audit burden. Integrating controls at the development stage shortens audit cycles and reduces the frequency of auditor requests. Teams that treat compliance as a post-deployment activity spend significantly more time responding to findings than teams that build controls into their delivery process from the start.

Automated evidence collection is the second pillar of a mature compliance programme. Timestamped, immutable records enable direct auditor access and faster validation. Manual evidence assembly is not only slow; it introduces transcription errors and version control risks that automated systems eliminate entirely. Connecting your asset auditing processes to your ITSM platform creates a single, queryable record of device state, ownership, and location that satisfies both operational and audit requirements.

The following practices define the current standard for financial IT compliance programmes:

- Continuous control monitoring: replace annual assessments with real-time dashboards that surface control failures as they occur

- Policy review cadence: schedule formal policy reviews at least annually, and trigger ad hoc reviews whenever a material regulatory change occurs

- Audit collaboration: involve internal audit teams in control design, not just control testing. Early involvement reduces the gap between what IT builds and what auditors expect to see

- Least privilege enforcement: automate access provisioning and deprovisioning workflows so that role changes and departures trigger immediate access updates without manual intervention

The table below summarises the control areas, their audit evidence requirements, and the recommended review frequency for financial IT compliance teams:

| Control area | Evidence required | Review frequency |

|---|---|---|

| Logical access | Access logs, provisioning records, review sign-offs | Quarterly |

| Change management | Change tickets, test results, approval records | Per change |

| Log retention | Archived system logs with integrity verification | Continuous, 7-year retention |

| SaaS inventory | Approved application register, access reviews | Quarterly |

| Segregation of duties | Role matrix, conflict reports, remediation records | Quarterly |

Compliance requires a shift from static checklists to dynamic, risk-based frameworks that link technical controls directly to regulatory obligations. In API-driven financial ecosystems, that linkage must be maintained programmatically, not through spreadsheets. Automation in compliance tooling now makes this achievable for teams of all sizes, not just those with dedicated GRC platforms.

Key takeaways

Financial services IT compliance requires continuous control monitoring, quarterly access reviews, and automated evidence collection to meet SOX, NIST SP 800-53 Rev 5, and FCA audit standards throughout the financial year.

| Point | Details |

|---|---|

| ITGCs are the foundation | Logical access, change management, system operations, and data centre security underpin every major financial regulation. |

| Quarterly reviews are mandatory | Auditors expect access reviews every quarter, not annually. Annual reviews create privilege creep and audit findings. |

| Log retention spans seven years | SOX requires system logs retained for up to seven years. Default 90-day cloud retention settings are a common audit failure. |

| RegTech enables continuous monitoring | Advanced platforms monitor millions of regulatory data points in real time, replacing manual obligation tracking. |

| Embed controls early | Integrating ITGCs in the development lifecycle reduces audit cycle times and the volume of auditor requests. |

The compliance function has outgrown the audit calendar

My view, shaped by years of watching financial IT teams prepare for audits, is that the biggest structural problem in financial services IT compliance is not a lack of controls. It is a mismatch between the pace of technology change and the pace of compliance governance.

Teams build controls for the IT environment that existed when the framework was last reviewed. Six months later, three new SaaS applications are in production, a CI/CD pipeline has been deployed, and a cloud migration has moved two financial systems to a new hosting environment. The controls are still pointing at the old architecture. The auditor arrives and finds gaps that were not gaps when the controls were designed.

The organisations that handle this well do one thing differently: they treat the IT asset register as a live compliance input, not a static inventory. Every change to the IT estate triggers a control review, not just a change management ticket. That discipline is harder to build than any individual control, but it is the difference between a clean audit and a findings letter.

The RegTech market is moving in the right direction. Automated obligation mapping and real-time control monitoring are genuinely useful. But the technology only works if the underlying data, asset records, access logs, change history, is accurate and current. That is still a people and process problem before it is a technology problem. The AI integration strategies entering financial IT in 2026 will accelerate the automation layer, but they will not substitute for the governance discipline that keeps the underlying data trustworthy.

— Anthony

How Velocity-smart supports financial IT compliance programmes

Financial IT compliance teams carry a disproportionate audit burden when device lifecycle data sits outside their core ITSM platform. Velocity-smart addresses this directly. The Smart Collect platform runs natively inside ServiceNow, recording every device handover, access event, and asset state change as a native CMDB record. That data is queryable, timestamped, and immutable, which means it satisfies audit evidence requirements without manual assembly.

For financial services organisations managing distributed IT estates across multiple sites, Velocity-smart’s automation solutions reduce the gap between physical asset activity and the audit trail that compliance teams need. Device location, ownership history, and handover records are captured automatically, removing a category of manual evidence collection that typically consumes significant IT staff time before each audit cycle. Explore how enterprise IT teams are automating IT hardware support to reduce compliance overhead and improve audit readiness across complex, multi-site financial environments.

FAQ

What is financial services IT compliance?

Financial services IT compliance is the practice of implementing and evidencing IT general controls (ITGCs) to meet the regulatory requirements governing financial data integrity, security, and auditability. Key frameworks include SOX Section 404, NIST SP 800-53 Rev 5, FCA rules, PCI DSS, and GDPR.

What does SOX Section 404 require from IT teams?

SOX Section 404 requires IT teams to document, test, and continuously validate Internal Controls over Financial Reporting for every system that processes financial data. This includes ERP platforms, billing systems, and revenue recognition tools.

How often should access reviews be conducted under SOX?

Auditors expect quarterly access reviews to verify adherence to the principle of least privilege. Annual reviews are a common control deficiency and frequently result in audit findings.

How long must system logs be retained for SOX compliance?

SOX requires system logs to be retained securely for up to seven years. Many organisations retain logs for only 90 days due to default cloud storage configurations, which creates a significant audit evidence gap.

What is the role of RegTech in IT compliance in finance?

RegTech platforms automate obligation-to-control mapping and monitor regulatory data points in real time across multiple jurisdictions. They reduce audit fatigue, surface control failures proactively, and give IT compliance teams lead time to respond to regulatory changes.

Recommended

See what Smart Collect® could save you

Model your savings in two minutes, or book a 60-minute workshop to pressure-test the numbers against your estate.